A nice trifecta of factors is telling investors that energy stocks are a buy: Investors hate them; insiders love them. And they’re cheap.

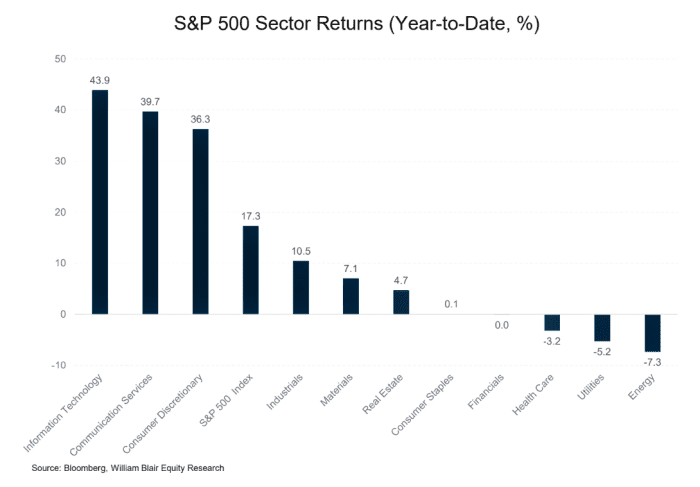

Energy is the U.S. stock market’s worst-performing group year to date. It stands out as the only cyclical group in the dumps.

Moreover, corporate insiders are buying the pullback. The energy sector saw the most corporate-insider buying the most relative to selling earlier in July, according to Vickers Weekly Insider published by Argus. Argus cited Texas Pacific Land Corp.

TPL,

Plus, energy stocks are cheap. Many energy stocks trade at 30% to 80% discounts to their five-year average price-to-earnings ratio. You see this across market caps. Exxon Mobil

XOM,

As for smaller names, two energy stocks recently suggested in my stock letter are up 20% since then, but they still look cheap. Matador Resources

MTDR,

“The space continues to trade at the low end of its historical range,” says Ben Cook, portfolio manager of the Hennessy BP Midstream Fund

HMSFX,

Reasons to be bullish

Here are two reasons why energy stocks will advance from here.

First, energy prices are going up. OPEC+ has been cutting production to boost oil prices, to no avail. Here’s why those cuts have not had a big impact — at least so far. Oil supply has been up a lot because of record U.S. strategic petroleum reserve (SPR) releases and upside production surprises from U.S. companies and sanctioned producers in Russia and Iran, says Goldman Sachs analyst Bruce Callum.

Callum says the SPR and the U.S. production headwinds will turn into moderate tailwinds as the SPR gradually refills and U.S. supply growth slows. Supply growth is impaired because global oil investment was 40% lower last year than in 2014. Cullen says an energy deficit in the second half should push Brent oil

BRN00,

Cook, at the Hennessy BP Midstream Fund, agrees. The supply-demand balance will shift in the second half of this year and next, he says, driving oil prices higher. “If you believe the global economy will hold up, and we do, we will be in deficit and prices will be elevated,” Cook says. He sees West Texas Intermediate trading at between $80 and $100 later this year and in 2024, versus a recent $79.

Medium term, look for the same price trend, says value investor William Nygren, who manages the Oakmark Investor Fund

OAKMX,

Read: 6 cheap stocks that famed value-fund manager Bill Nygren says can help you beat the market

As for natural gas, the U.S. Energy Information Agency estimates global liquid natural gas demand will roughly double to 700 million tons per annum (MPTA) by 2040 from 380 MPTA in 2021. Baker Hughes

BKR,

Second, the renewables overhang may fade. Many investors avoid energy stocks on fears that renewables will ramp up sharply, displacing fossil fuels. This is unlikely. The media and other commentators are overestimating how fast alternative fuel sources will come on line, Nygren says. This misperception should drive investor interest in energy stocks.

Besides, history shows that even when the most popular fuel sources (like wood and coal) get replaced by new sources, we still use more of the displaced fuels years later, compared to when they were the top fuel in use, Nygren says. “It is reasonable to think that fossil fuels go the same way.”

Energy stocks to consider

Nygren owns three main energy companies in his fund. They are EOG Resources

EOG,

1. A long runway of underappreciated inventory in the form of untapped energy assets in the ground. “That’s less capital they will have to spend to replace assets and grow their businesses,” says Nygren.

2. These companies are lower-cost producers but are not rewarded for this, since they trade at about an industry multiple.

3. They are returning cash to shareholders via buybacks and dividends. For example, EOG pays a 2.7% yield, COP pays a 4.7% yield and APA pays a 2.6% yield. “The willingness of management to return capital to shareholders is a very important characteristic for us,” Nygren says. “Over the next 10 years, we believe ConocoPhillips will be able to return over 100% of its current market capitalization to shareholders via dividends and share repurchases while growing its production at a mid-single-digit annual pace.”

4. The shares look cheap. On a trailing p/e basis, EOG trades at a 63% discount, ConocoPhillips goes for a 36% discount APA trades at an 82% discount to its trailing five-year average.

Two energy income plays

A safer way to invest in energy is to own the midstream pipeline and infrastructure companies. These companies earn a fee for gathering and transporting fuel to energy hubs. So, they are much less exposed to energy price volatility than producers. But they can see earnings growth as volumes pick up.

A simple way to get diversified exposure to this group would be to own the Hennessy BP Midstream Investor Fund. It outperforms competing funds by four percentage points, annualized, over the past three years, according to Morningstar Direct. The trailing 12-month yield is 10.65%, Morningstar reports.

Cook singled out Plains GP Holdings

PAGP,

Since the company’s network connects Permian producers to the Gulf Coast, it stands out as a big beneficiary of increasing foreign demand for U.S. oil and natural gas. As geopolitical tensions rise, foreign energy buyers value U.S. producers even more as transparent, and reliable suppliers. This boosts demand for U.S. energy.

Michael Brush is a columnist for MarketWatch. At the time of publication, he owned TPL, MTDR, CRK and EOG. Brush has suggested TPL, OXY, XOM, MTDR, CRK, EOG, APA, COP and PAGP in his stock newsletter, Brush Up on Stocks. Follow him on X (formerly Twitter) @mbrushstocks

More: Why are gas prices going up again? Brace for further increases, analysts say

Also read: Feds propose 18% fuel-economy increase — to 43.5 MPG — for new vehicles by 2032